(Editor’s note – This article on the status of rooftop solar PV in India and the comparison of state rooftop policies appeared in the April 2013 print edition of PV-Magazine and the May 2013 edition of the Chinese edition of PV-Magazine. The article was written by Madhavan Nampoothiri, Director of RESolve. Click here to read the original article available for subscribers)

2012 was a momentous year for Solar in India. In July 2012, the total installed capacity of solar power generation projects crossed 1 GW, mainly propelled by the state of Gujarat’s solar policy(more than 700 MW) and by the federal government policy – Jawaharlal Nehru National Solar Mission(JNNSM) (about 300 MW). The notable part about this 1 GW achievement is that almost all these projects are ground-mounted utility scale grid-connected systems. This compares to a market share of about 15% for ground-mounted systems in Germany in 2011(Source BSW).

While installing large scale projects help in achieving the capacity addition targets faster, small scale rooftop PV systems have some very obvious advantages.

- No additional land that could be used for other purposes is required for rooftop PV systems.

- Huge savings in the Transmission and Distribution losses. In India, T&D losses are as high as 32%.

- Diesel consumption offset – In India, rampant power cuts are a norm and the scheduled outages can be as high as 16 hours a day in some parts of the country. During the outages, industries, commercial establishments and residential consumers who are affluent, tend to use diesel generators. Power from diesel generators is not only expensive, but also leads to pollution.

- Solar PV rooftop systems can also reduce the reliance of the power grid.

- Local employment generation

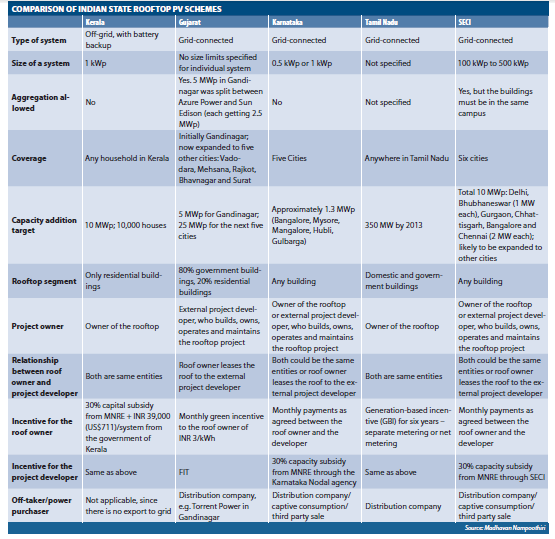

According to officials of Ministry for New and Renewable Energy (MNRE), the potential of rooftop PV systems could be at least 20 GW. In December 2012, MNRE released a policy document draft regarding the next phase of the solar mission. One of the areas that the policy document stresses upon is the rooftop PV segment, with a possible deployment of upto 1 GW of rooftop projects – both at off-grid and grid-connected levels. While MNRE has not finalised the plans at the time of writing this article, the newly formed organisation – Solar Energy Corporation of India (SECI) – has already started the process to allocate 10 MW of rooftop PV projects in 6 cities – Delhi, Bhubhaneswar (1 MW each) in Orissa, Gurgaon in Haryana, Raipur in Chhattisgarh, Bangalore in Karnataka and Chennai in Tamil Nadu (2 MW each). SECI will incentivise the rooftop project owners by giving 30% capital subsidy.(Update: SECI has allocated projects to companies Sun Edison, Azure and Thermax. Click here for more).

Apart from SECI, several state governments have initiated rooftop PV programmes specific to their respective states. Not surprisingly, the pioneer in the deployment of solar PV rooftop programme is the state of Gujarat. The state allotted 5 MW of rooftop projects to 2 companies – Azure Power and Sun Edison last year and has announced its plans to expand the programme to 5 more cities in the state totalling 25 MW in capacity.

While the rooftop PV projects in Gujarat are all grid-connected and based on a Feed-in-Tariff (FiT), the Southern state of Kerala has taken a different approach. It has announced a policy for the deployment of 10,000 off-grid systems across the state. The policy by Kerala is reminiscent of the 1000 rooftop programme started in the 1990s by Germany. The off-grid systems under the 10,000 rooftop programme in Kerala will be of 1 kW size each, and comes with battery storage. Instead of a FiT, the project owners will get upfront capital subsidies. Another difference between the Gujarat policy and the Kerala policy is that in case of the former, the allocation is given to 2 large developers, whereas in Kerala, the allocation is given to 10,000 individual households. (A comparison of Gujarat and Kerala rooftop schemes is available here).

Two other South Indian states – Tamil Nadu and Karnataka has also announced policies to promote rooftop PV. In case of Tamil Nadu, the state policy targets 350 MW of rooftop installations by 2015, out of which 50 MW will on residential rooftops. The state has proposed a Generation Based Incentive, which is similar to the FiT. The state is also exploring the option of implementing net metering for these rooftop projects.

Karnataka’s rooftop PV programme targets about 1.2 MW of rooftop installations and has started the project allocation process. This programme is quite similar to Gujarat in the sense that the programme is administered across 5 cities in Karnataka and will be grid connected. The project sizes are very small (0.5 kW and 1 kW) with the government providing capital subsidy. A comparison of the rooftop projects under different state policies are given below. (Click on the image to enlarge it).

Challenges

1. Financial – The high upfront investment is often a major deterrent in rooftop PV deployment.

2. Regulatory/policy

- At present, only capital subsidies and tax benefits in the form of accelerated depreciation are provided for PV systems (up to 500kWp).

- The process of getting approval for the projects and getting the capital subsidy disbursed takes long time. The slow turn-around times and some uncertainty about getting the payments is a challenge in adoption of the rooftop PV.

3. Infrastructural

Implementing a Feed-in-Tariff system for rooftop PV, along the lines of major European countries, is a powerful mechanism to stimulate growth in this segment. However, challenges like prevention of abuse of the mechanism like feeding in power to the grid from cheaper source of power (perhaps subsidized kerosene) and getting higher feed-in-tariff needs to be addressed in order to make this model successful. In fact, the Government of Delhi had to scrap its rooftop policy because of the perceived challenge in this area.

In addition to these issues, Pune based Think-tank Prayas group has come up with a study that highlights the challenges in implementing a Feed-in-Tariff approach which include:

- Higher burden on utility – due to the smaller sizes of rooftop PV (RTPV), the unit cost of electricity from these systems tend to be higher, making power purchase from them uncompetitive in comparison to power purchase from utility scale projects.

- Difficulty in estimating FiT – With the rapid fall in PV system prices, arriving at a FiT has been a challenge not only for utility scale projects, but also for RTPV.

The study argues that due to these challenges in the FiT based approach, a net-metering based approach, as adapted by the Tamil Nadu Solar policy should be promoted. In order to promote net-metering, the study recommends the following steps.

- Progressively increase the tariff for high-end consumption in residential and commercial sectors, thereby bringing RTPV power generation cost close to the price of grid-electricity.

- Provide interconnection to the grid and banking facility for rooftop PV systems.

- Instead of providing payouts for the net electricity exported to the grid, the credit can be rolled over to the next billing cycle and upto a year.

4. Availability of rooftop – While the number of rooftops in the country is very high, a big part of them are not suitable for installing PV systems.

5. Other Challenges

- Structural Constraints: Roofs of a certain age or construction may be less desirable for a solar installation and may require a significant refurbishment before such an installation is possible. Ideal conditions include roofs with 10-20 years remaining before significant maintenance or overhaul is required.

- Limit on single phase generation: If there are many such micro generators (as we can call small solar PV panel installations) and their supply is not balanced among the phases, the network can become imbalanced.

- Quality of electricity: There are strict criteria so that having multiple generation sources does not impact the quality of electricity available in the grid. This includes the issue of harmonics (distortion of the Sine wave AC signal) and EMC (Electromagnetic Compatibility) requirements.

While the utility scale solar sector is posting significant growth across the country, rooftop solar is definitely the buzzword. The significant opportunity presented by the energy deficit and escalating energy costs in various pockets of the country coupled with the need for energy security for not only large business but also home owners, the small scale solar segment promises to be the next big thing in the solar space in India, provided the challenges presented are surmounted.

___________________________________________________________________________________________

Subscribe to RESolve Energy Consultants : Perspectives and Insights by Email

___________________________________________________________________________________________

The cost of generation from Rooftop PV are approaching fast towards grid parity. In such scenario, FiT and subsidy on capital cost should be avoided for the financial health of the governments,since it is difficult to withdraw facilities once given. The governments should encourage for soft loans only.For implementation of net metering, the study should be conducted whether Discoms/Distribution utilities will be able to stabilize their distribution system with induction of large number of rooftop solar PV. The Discoms/Distribution utilities should be capable for effective metering, proper billing, timely collection of revenue. There is need to implement rooftop PV system after detailed study and implement in phased manner for smooth operation of system.