MNRE today released the total solar installed capacity in the country – the number stood at 2631.9 MW as of 31 March 2013. That represents an increase of 948 MW from the previous financial year(FY).

The growth trajectory for the past years can be seen below.

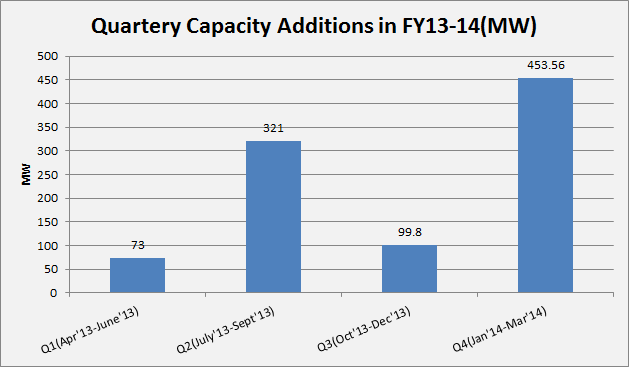

Earlier in January 2014, when MNRE had previously published the data, the total installed capacity stood at 2206.75 MW(read more here). An astonishing, 425.2 MW of solar PV capacity has been added in the last two months of the financial year ending in March 2014. In all likelihood, the 3 GW barrier will be breached this year as a result of the various state solar initiatives.

The quarterly capacity additions are given below. The capacity addition has been the highest in the last quarter, and the numbers suggest that the additions could be by companies who developed the projects to claim the Accelerated Depreciation(AD) benefits by the end of March 2014. These projects would be mainly under the REC mechanism (Since AD is no longer available for wind projects, many of them turned to solar to claim the AD benefits).

In terms of installed capacity by state, it should come as no surprise that Gujarat tops the list with an installed capacity of 916.4 MW followed by Rajasthan (730.1 MW), Madhya Pradesh (347.2 MW) and Maharashtra (249.3 MW). It may be recalled that in the numbers released in January 2014, Maharasthra was ahead of Madhya Pradesh, but Madhya Pradesh is likely to retain its position in the Top 3 states for the foreseeable future. (Madhya Pradesh bagged one third of the projects under the JNNSM Phase 2, Batch 1).

It is interesting to note that the capacity addition in each state has been driven by different measure. The mammoth total in Gujarat has been driven by the state’s (then) innovative solar policy while those in Rajasthan has been a result of the National Solar Mission. Madhya Pradesh has leapfrogged Maharashtra in the standings to take the third place through capacity additions under both state schemes as well as the REC mechanism.

REC which has long been neglected has seen a resurgence this financial year. About 200 MW of REC based projects have come up in the last two months alone with REC projects accounting for about 19% of the total installed capacity in the country. REC based projects have been the driving force behind capacity addition in various states such as Tamil Nadu, Madhya Pradesh and Maharashtra where REC projects account for about 80%, 48% and 20% of the total installed capacity.

The impact of REC based projects is most evident in Tamil Nadu where the state’s solar policy has been in limbo for the past year and developers eager to setup projects in the state have moved on to the REC mechanism to ensure that projects take off. Another reason could be the fact that REC projects can take advantage of the accelerated depreciation (AD) benefit. The profitability of REC based projects however still remains uncertain due the uncertain nature of the REC market itself where the solar RECs have been trading at the floor price for a long time with inventories piling up due to lack of buyers.

Future capacity additions in the country are very likely to be driven as always by the state specific solar policies complemented by the National Solar Mission. Should the various projects under the state policies come up on schedule, the 3 GW mark could very well be breached this year.

The details can be downloaded from the MNRE website here.

Subscribe to RESolve Energy Consultants : Perspectives and Insights by Email

______________________________________________________________________________________________

I think that there are several discrepancies in the data published. First of all the last quarter numbers are not what you state because I think at least 55 MW of CSP has been added to the PV number. This CSP is not from last quarter. Also, 50 MW RPO project in Gujarat is the Torrent Power 50 MW project being executed by Hindustan Clean Energy. As far as I know, that project has not been commissioned yet.

Mahagenco project is 125 MW. Welspun 25 MW project for BEST, that can take the Maharashtra tally to 150 MW has also not been commissioned.

We got a list from Madhya Pradesh about commissioned projects on 20th of last months, stating the total capacity at 257 MW. MNRE has stated 347 MW for Madhya Pradesh.

Is there something we are missing? Have you confirmed this data and subsequent analysis?

I think that the total installed capacity should be 2.3 GW, including CSP.

@Jasmeet – First of all, I agree with your sentiment about the MNRE numbers. We were quite surprised at the last quarter addition which is higher than what we had estimated. We were also pleasantly surprised that the data was made available on 1st day of the new FY(which is unusual for a Ministry). Having said that, this analysis is purely based on the MNRE numbers. If we get concrete information which contradicts the MNRE numbers, we will update the analysis accordingly.

Thanks for sharing your views!!

Madhavan

Thanks for the efforts!

I think the most interesting part of your analysis is the pie chart in the end. Its wonderful to see states (some of them) walking the extra mile for solar gains. Tamil Nadu could and should have been a part of the solar club but…

Thanks, Anand. Tamil Nadu can still go ahead of most other states if it signs the PPA for the 700 MW odd capacity for which LOI has already been given.

Good info , Thanks

Kumar

Zynergy